Improving Cash Flow Forecasting with Analytics

Historically, cash flow forecasting was a reactive process:

accounting teams looked at past invoices and bank statements, made educated

guesses about collection timelines, and put together static spreadsheets that

were outdated the moment they were saved.

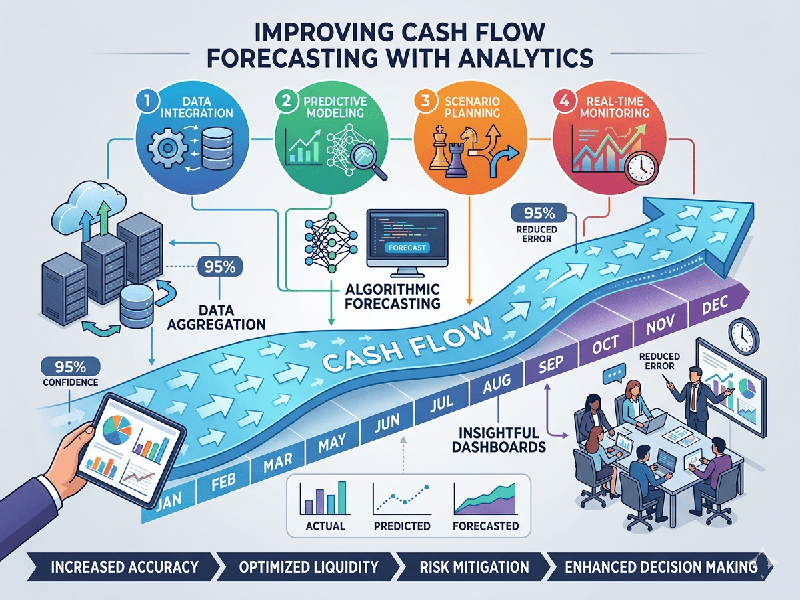

By replacing manual entry with integrated data pipelines and

predictive analytics, enterprises shift from historical reporting to

proactive cash management. This allows finance teams to optimize working

capital, negotiate better credit terms, and strategically time capital

expenditures (CapEx).

1. Transforming the Cash Flow Framework

Moving from traditional to predictive analytics requires

upgrading how data is collected, consolidated, and processed across business

units.

- Real-Time Data Integration: Instead of waiting for monthly

reconciliations, automated analytics engines pull daily transaction data

directly from bank feeds, accounts receivable (AR), accounts payable (AP),

and sales pipelines.

- Dynamic DSO & DPO

Calculation:

Instead of assuming a flat 30-day payment cycle, analytics engines track

actual historical behavior to assign dynamic Days Sales Outstanding

(DSO) metrics down to individual clients and Days Payable

Outstanding (DPO) trends to specific vendors.

2. Advanced Analytics Techniques for Cash Optimization

Implementing advanced analytics allows finance teams to

uncover hidden liquidity and anticipate shortfalls weeks before they happen.

Statistical and Predictive Modeling

Traditional forecasts struggle with nuance. By applying

time-series forecasting models (like ARIMA or Prophet), analytics software can

parse years of historical bank data to automatically identify hidden seasonal

dips, recurring quarterly operational expenses, and macro-economic payment

slow-downs.

Customer Payment Behavior Analytics

Not all clients stick strictly to their invoice terms.

Machine learning classification models can scan past invoice histories to

calculate a "Probability of Late Payment" score for open invoices. If

a major distributor consistently pays 12 days late during their regional

monsoon or financial off-season, the forecast automatically shifts that

expected inflow out by 12 days.

Automated Scenario Simulation (Stress Testing)

Instead of manually tweaking cells in a spreadsheet, variance

engines run automated Monte Carlo simulations to test how cash positions would

respond to sudden market changes.

Example Scenario Analysis: What happens to our net cash position if our top supplier raises material costs by 8%, raw material shipping times slow down by 14 days, and a major customer delays a ₹10,000,000 payment by two weeks?