Fraud Prevention in eCommerce

Fraud prevention in eCommerce requires a

multi-layered, proactive strategy that balances security with a seamless

customer experience. In the 2026 landscape, the focus has shifted toward

adaptive, AI-driven systems that move beyond static rules to identify complex,

evolving threats.

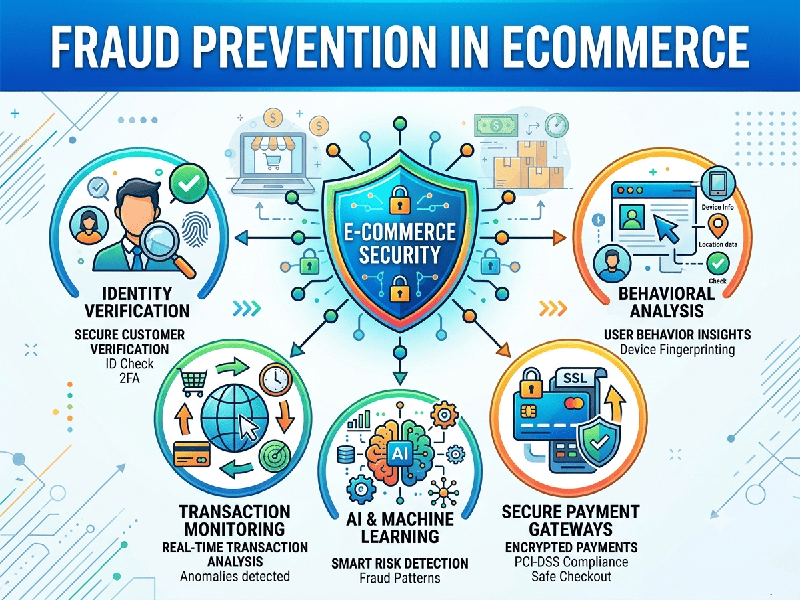

1. Foundational Security Layers

- Multi-Factor Authentication

(MFA):

Essential for account security. Implement OTPs, authenticator apps, or

biometrics to verify identity during logins and high-risk transactions.

- Payment Security: Ensure full compliance with PCI

DSS standards. Utilize 3D Secure 2.0 for payments, as it provides

risk-based authentication, applying friction (like an additional check)

only when a transaction is flagged as suspicious.

- Data Protection: Use SSL/TLS encryption for all

data in transit to prevent interception. Regularly audit your platforms to

remove inactive plugins and patch security vulnerabilities.

2. Advanced Detection & Prevention Technologies

- AI & Machine Learning (ML): Modern platforms use ML to

analyze thousands of data points in real-time, such as device

fingerprinting, behavioral patterns, and network reputation. This helps

catch "card-not-present" (CNP) fraud that rule-based systems

often miss.

- Behavioral Analytics: Monitor how users interact with

your site. Indicators like non-human mouse movements, unusual typing

rhythms, or rapid device switching often signal bot-driven attacks or

account takeover attempts.

- Velocity Checks: Automatically flag or block

accounts/IP addresses that exhibit suspicious behavior, such as multiple

failed login attempts or a high volume of purchases in a very short

timeframe.

- Device Fingerprinting: Create unique identifiers for

devices based on browser, OS, and hardware settings to track returning bad

actors, even if they attempt to mask their identity using VPNs or proxy

servers.

3. Contextual Strategies for the Indian Market

Given the specific regulatory and operational

environment in India:

- Merchant Verification: If you operate a marketplace,

rigorous onboarding is your first line of defense. Verify business

identity using GSTIN lookups, MCA21/CIN checks, and matching registered

business addresses against digital signals.

- OTP-Based Delivery: For high-value or sensitive

orders, adopt an "OTP for delivery" model (similar to Amazon

India) to ensure the physical receipt matches the account holder.

- Regulatory Compliance: Ensure all payment aggregation

follows RBI guidelines, including periodic merchant due diligence and

transaction monitoring to prevent settlement risks.

4. Operational Best Practices

- Progressive Friction: Don't treat every user as a

suspect. Start with low-friction checkout and introduce

"step-up" authentication (e.g., an extra verification step) only

when a transaction's risk score crosses a certain threshold.

- Human-in-the-Loop: Balance automation with expert

review. Aim for a 30%–60% review-then-decline rate; if you are

declining far more than that automatically, you may be losing legitimate

revenue.

- Chargeback Management: Keep meticulous digital

logs—shipping confirmations, IP logs, and customer communication

records—to successfully contest "friendly fraud" (when a

customer claims they didn't authorize a charge).

5. Key Metrics for Success

Evaluate your fraud prevention platform based on three

concurrent metrics:

1.

Fraud Loss Reduction: The primary goal.

2.

False Positive Rate: Ensure legitimate customers aren't being blocked.

3.

Authorization Lift: A good system should actually improve your ability to approve valid

orders by providing issuers with more confidence in your traffic.