Designing Secure Payment Gateways

Designing a secure payment gateway requires a multi-layered

defense strategy that balances strict security protocols with a frictionless

user experience. In the modern fintech landscape, security is not just about

encryption; it is about establishing a "Chain of Trust" from the

moment a user enters their card details until the funds are settled.

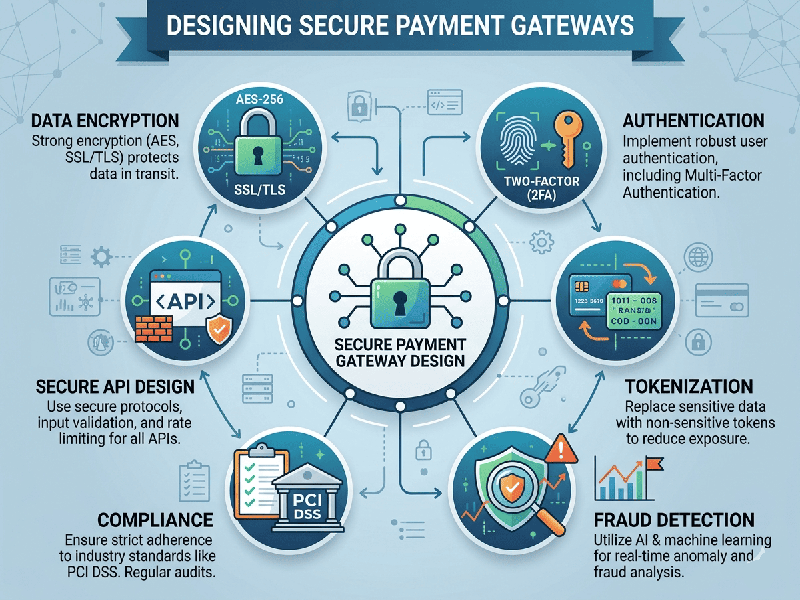

1. Core Security Architecture

A secure gateway must adhere to several industry-standard

architectural principles to protect sensitive financial data.

- PCI-DSS Compliance: The Payment Card Industry Data

Security Standard is the baseline requirement. It mandates a secure

network, protected cardholder data, and regular monitoring of systems.

- Tokenization: This is the most critical

defense. Instead of storing the Primary Account Number (PAN), the gateway

replaces it with a unique, randomly generated "token." Even if a

database is breached, the tokens are useless to hackers.

- End-to-End Encryption (E2EE): Data must be encrypted at the

point of entry (the browser or app) and remain encrypted until it reaches

the secure processing environment.

2. Authentication and Verification

Verification steps ensure that the person initiating the

transaction is the actual owner of the payment instrument.

- 3D Secure 2.0 (3DS2): This provides an extra layer of

authentication (like a biometric check or a one-time password) without

necessarily interrupting the checkout flow, using data sharing to verify

identity.

- AVS (Address Verification

System): Compares

the billing address provided by the user with the address on file with the

credit card issuer.

- CVV/CVC Checks: Ensuring the physical card is

present by requiring the 3-digit code on the back.

3. The Transaction Flow

Understanding how a secure transaction moves through various

entities is vital for identifying potential points of failure.

1.

Initiation:

The user enters card details on a secure, TLS-encrypted form.

2.

Authorization Request: The gateway encrypts the data and sends it to the acquiring

bank (the merchant's bank).

3.

Authentication:

The acquiring bank forwards the request to the issuing bank (the customer's

bank) via card networks (Visa/Mastercard).

4.

Verification:

The issuing bank checks for fraud and sufficient funds.

5.

Response: The

"Approved" or "Declined" status is sent back through the

gateway to the merchant.

4. Fraud Prevention & Risk Management

Modern gateways utilize real-time analysis to stop fraudulent

attempts before they are processed.

- Velocity Checks: Monitoring for

"carding" attacks, where a bot attempts hundreds of small

transactions in a few minutes to see which cards are active.

- Geolocation & IP Filtering: Flagging transactions that

originate from high-risk regions or IPs associated with previous fraud.

- Behavioral Analytics: Using machine learning to

detect if a transaction deviates from a user’s typical spending habits.